Note

Go to the end to download the full example code.

TradLife_A_EX1: SCR shock cashflows#

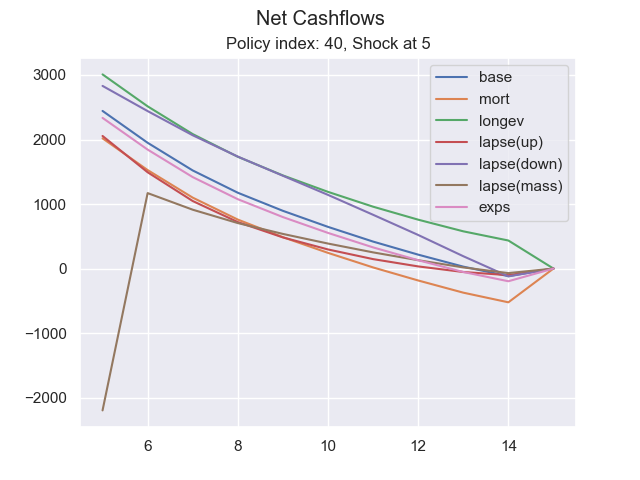

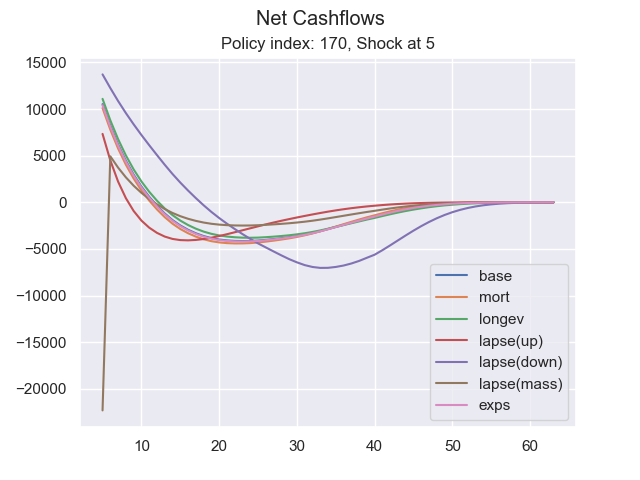

Net liability cashflows under the prescribed Solvency II life shock

scenarios for selected policies, projected by the annuallife

TradLife_A_EX1 model.

For each policy the inner projection InnerProj[t0, risk, shock] is

re-run from the valuation time t0 under every life stress, and the

per-period net cashflow net_cf is charted from t0 to the end of

the projection. The mass-lapse line drops sharply at t0 because a

fraction of the policies surrenders instantly under that shock.

See also

The

annuallifelibrary

import modelx as mx

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_theme(style="darkgrid")

model = mx.read_model("TradLife_A_EX1")

LifeRiskID = model.Enums.LifeRiskID

LapseShockID = model.Enums.LapseShockID

# (label, risk, shock) for each prescribed life stress

scenarios = [

('base', LifeRiskID.BASE, 0),

('mort', LifeRiskID.MORT, 0),

('longev', LifeRiskID.LONGV, 0),

('lapse(up)', LifeRiskID.LAPSE, LapseShockID.UP),

('lapse(down)', LifeRiskID.LAPSE, LapseShockID.DOWN),

('lapse(mass)', LifeRiskID.LAPSE, LapseShockID.MASS),

('exps', LifeRiskID.EXPS, 0),

]

def draw(idx, t0):

fig, ax = plt.subplots()

fig.suptitle('Net Cashflows')

title = 'Policy index: ' + str(idx) + ', Shock at ' + str(t0)

proj = model.Projection[idx]

last_t = proj.proj_len()

data = {}

for label, risk, shock in scenarios:

inner = proj.InnerProj[t0, risk, shock]

data[label] = [inner.net_cf(t) for t in range(t0, last_t + 1)]

return pd.DataFrame(

data, index=range(t0, last_t + 1)).plot(

ax=ax, kind='line', title=title)

# idx 40 / 170 correspond to PolicyID 41 / 171 in simplelife (0-based).

for idx, t0 in [(40, 5), (170, 5)]:

draw(idx, t0)

Total running time of the script: (0 minutes 0.814 seconds)